Business Compliance in 2026: Key Regulatory Changes

(and What They Mean for Your Finances, Payroll and Bookkeeping)

The UK compliance landscape has entered one of its most transformative periods in recent years. Across tax, payroll, and financial reporting, 2026 marks a decisive shift toward real-time reporting, digital record-keeping, and increased regulatory scrutiny.

For business owners, finance teams, and advisers, this isn’t just another annual update. It represents a structural change in how financial data is recorded, reported, and reviewed. The businesses that adapt early will find themselves operating more efficiently and with greater visibility. Those that don’t risk falling behind, both operationally and in terms of compliance.

In this article, we explore the most important regulatory developments shaping 2026 and what they mean in practice.

The shift to digital-first compliance

One of the defining themes of 2026 is the continued move toward digital compliance systems. HMRC and other regulators are increasingly prioritising accuracy, transparency, and accessibility of financial data, which means manual processes and fragmented systems are becoming harder to justify.

This shift is not just about convenience. It’s about reducing errors, improving audit trails, and enabling more frequent reporting. As a result, businesses are expected to maintain digital records that can be shared and reviewed in near real-time, rather than relying on retrospective, year-end processes.

For many organisations, this requires a rethink of internal processes. Bookkeeping, payroll, and tax reporting are no longer separate silos—they are becoming part of a connected compliance ecosystem.

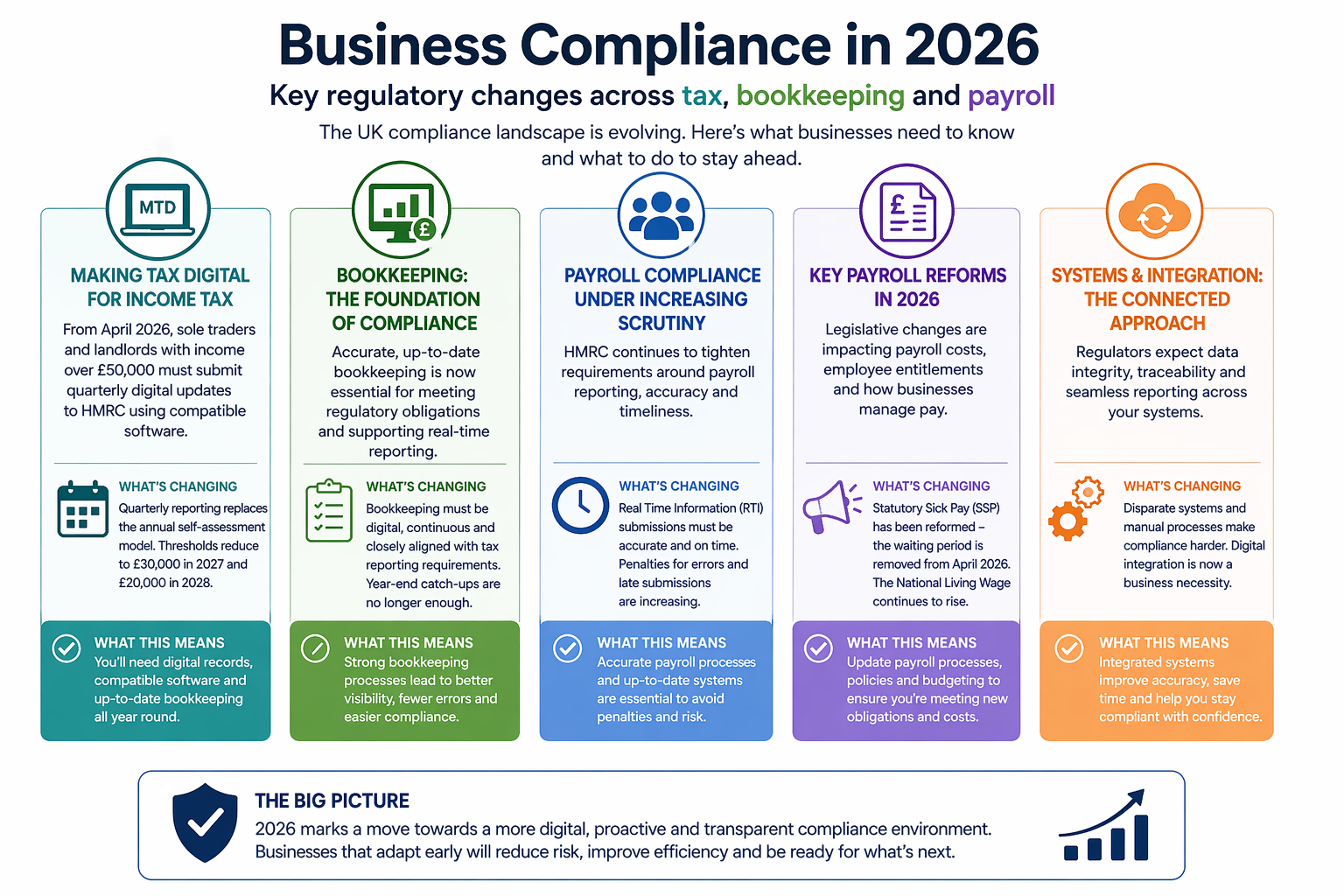

Making Tax Digital: a fundamental change to tax reporting

The rollout of Making Tax Digital (MTD) for Income Tax is arguably the most significant regulatory development of the year.

From April 2026, sole traders and landlords earning over £50,000 are now required to submit quarterly digital updates to HMRC using compatible software, replacing the traditional annual self-assessment process.

This is not a temporary adjustment. It’s the beginning of a phased expansion that will bring more businesses into scope over the coming years, with thresholds expected to fall to £30,000 in 2027 and £20,000 by 2028.

In practical terms, this means:

Businesses must maintain digital records of income and expenses

Tax reporting becomes a year-round activity rather than an annual event

Software is no longer optional—it is a core compliance requirement

While the transition may feel burdensome initially, the long-term intention is to improve accuracy and reduce errors in tax reporting. However, it also places greater responsibility on businesses to ensure their bookkeeping processes are consistent, up to date, and digitally integrated.

Bookkeeping: from back-office function to compliance cornerstone

As MTD takes hold, bookkeeping is evolving from a routine administrative task into a critical compliance function.

Accurate, timely bookkeeping is now essential not just for financial visibility, but for meeting regulatory obligations. With quarterly submissions becoming the norm, businesses can no longer afford to “catch up” at the end of the year.

Instead, bookkeeping must be:

Continuous rather than periodic

Digitally maintained and software-driven

Closely aligned with tax reporting requirements

This shift is prompting many businesses to adopt cloud-based systems and automate data capture wherever possible. The benefit is not just compliance—it’s also improved decision-making, as financial data becomes more current and reliable.

Payroll compliance: increasing scrutiny and complexity

Alongside tax changes, payroll compliance is becoming more demanding in 2026.

HMRC continues to place significant emphasis on the accuracy and timeliness of Real Time Information (RTI) submissions. Employers are expected to report payroll data every time employees are paid, and enforcement around errors and late submissions is tightening.

At the same time, broader payroll changes are affecting how businesses manage their workforce:

Greater scrutiny of PAYE reporting and reconciliation

Increased expectations around data security and audit trails

Ongoing pressure to ensure payroll systems are aligned with tax rules and thresholds

There are also notable legislative updates affecting payroll calculations and costs. Employer National Insurance remains elevated, and the threshold at which contributions begin continues to impact a larger portion of employee earnings.

Meanwhile, wage increases—such as the rise in the National Living Wage—are adding further pressure to payroll budgets and forecasting.

Key payroll reforms to be aware of

One of the most notable operational changes in 2026 is the reform to Statutory Sick Pay (SSP).

From April 2026, SSP has undergone one of its most significant changes in decades, including the removal of the traditional waiting period, meaning payments can begin earlier for employees.

This is part of a broader trend toward strengthening worker protections and modernising employment practices. For employers, it introduces additional considerations in payroll calculations, absence tracking, and compliance processes.

At the same time, the overall payroll landscape is becoming more complex, with growing reporting requirements and increased regulatory oversight. Businesses are expected to maintain accurate records, ensure correct tax and National Insurance calculations, and be prepared for more frequent compliance checks.

Sources: HMRC – Making Tax Digital, GOV.UK

The growing importance of systems and integration

A recurring theme across all these changes is the need for integrated systems.

Disconnected tools and manual processes make it significantly harder to comply with modern requirements. Payroll, bookkeeping, and tax reporting systems must now work together seamlessly to ensure consistency and accuracy.

This is particularly important as regulators place more emphasis on data integrity and traceability. Businesses need to be able to demonstrate not just that their figures are correct, but how those figures were generated.

For many organisations, this means investing in:

Cloud-based accounting and payroll platforms

Automated data capture and reconciliation tools

Clear audit trails and reporting workflows

What this means for businesses

Taken together, the changes in 2026 represent a move toward a more proactive, digital, and transparent compliance environment.

Rather than viewing compliance as a periodic obligation, businesses must now treat it as an ongoing process embedded within daily operations.

Those that adapt effectively will benefit from:

Better financial visibility

Reduced risk of errors and penalties

More efficient reporting processes

Those that don’t may find themselves struggling with increased administrative burden, missed deadlines, and potential compliance issues.

Final thoughts

2026 is not just another year of incremental updates—it’s a turning point in how compliance works in the UK.

With Making Tax Digital reshaping tax reporting, payroll requirements becoming more rigorous, and bookkeeping moving to the centre of compliance, businesses must rethink how they manage their financial processes.

The good news is that, while the transition requires effort, it also creates an opportunity. By embracing digital systems and strengthening internal processes, businesses can not only stay compliant but also operate more effectively and with greater confidence.

Disclaimer

This article is intended for general informational purposes only and does not constitute professional advice. While every effort has been made to ensure the accuracy of the information at the time of writing, regulations and guidance may change. You should always seek advice from a qualified accountant, tax adviser, or payroll specialist before making decisions based on this content.