The Hidden Cost of Doing Your Own Bookkeeping

At first, doing your own bookkeeping can feel like the sensible option.

It saves money, gives you control, and seems manageable—especially in the early days of running a business.

But over time, what looks like a cost-saving decision can quietly become one of the most expensive choices you make.

Not always in obvious ways—but in time, stress, missed opportunities, and sometimes, costly mistakes.

It Starts Off Feeling Manageable

In the beginning, bookkeeping often feels straightforward.

You might track income in a spreadsheet, for example, or upload receipts as you go, logging into your accounting software every now and then.

And for a while, that works.

But as your business grows—even slightly—things start to change.

There are more transactions, more complexity, more deadlines. And suddenly, what used to take 30 minutes now takes hours.

The Time Cost Adds Up Faster Than You Think

Bookkeeping isn’t just data entry.

It’s:

Reconciling transactions

Matching payments to invoices

Chasing missing receipts

Fixing errors when things don’t quite add up

And often, it’s not done in one clean block—it’s done in bits, squeezed in between everything else.

An hour here. Two hours there. A rushed session before a deadline.

Over a month, that can easily add up to 10–15 hours or more.

That’s time that could be spent:

Bringing in new business

Supporting clients

Developing your services

At a certain point, the question becomes:

👉 Is this really the best use of your time?

The Stress Factor (That Often Goes Unnoticed)

One of the biggest hidden costs isn’t financial—it’s mental.

If bookkeeping is something you:

Put off

Rush through

Feel unsure about

…it creates a low-level, ongoing stress.

You might find yourself thinking:

“I need to catch up on that”

“I hope that’s right”

“I’ll deal with it later”

That uncertainty builds over time—and tends to peak around deadlines.

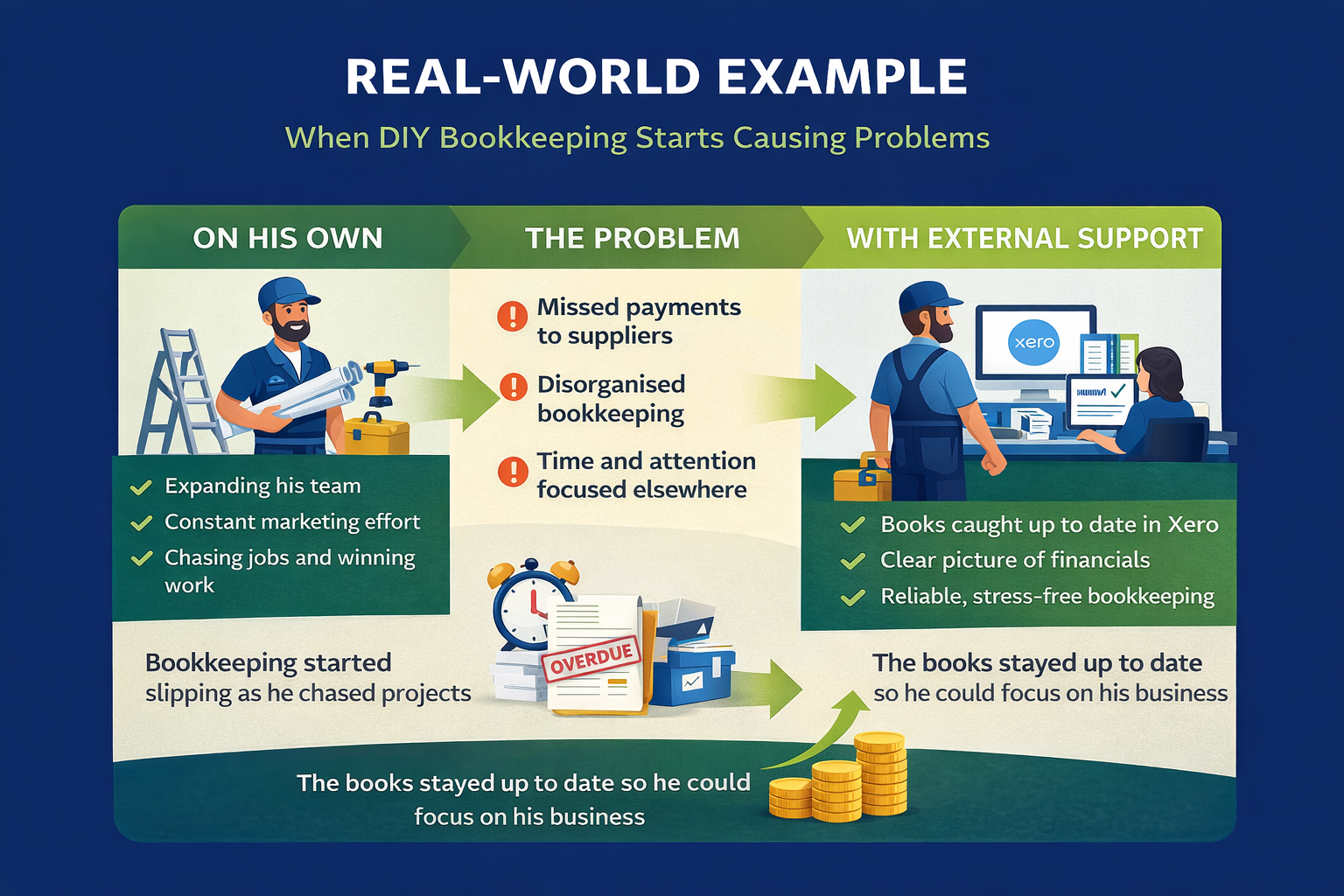

A Real-World Example

(Names and details have been changed for confidentiality.)

We worked with a sole trader in the trades who was doing exactly what you’d want to see in a growing business.

He was expanding his team, bringing in subcontractors, and actively marketing his services. Work was coming in, and the business was moving in the right direction.

But as his focus shifted towards winning and delivering work, the behind-the-scenes tasks—particularly bookkeeping—started to drift.

It wasn’t that there wasn’t enough money in the business.

The issue was time and attention.

Invoices weren’t always matched up, supplier payments were missed or delayed, and things began to feel disorganised. Not because the business wasn’t performing—but because the financial side wasn’t being kept on top of.

When they brought in external support, the focus was first on getting everything back on track—bringing the books up to date in Xero and creating a clear picture of where things stood.

From there, it became about consistency—keeping everything accurate, up to date, and working in support of the business rather than against it.

Having things organised and up to date removes that background noise—and gives you confidence that everything is under control.

Small Mistakes Can Turn Into Bigger Problems

Bookkeeping underpins everything—from your tax returns to your day-to-day decisions.

And when you’re doing it yourself, small errors are easy to make:

Misclassifying expenses

Missing transactions

Duplicating entries

Forgetting to reconcile accounts

Individually, these might seem minor.

But over time, they can lead to:

Incorrect tax calculations

Overpaying or underpaying HMRC

Complications at year-end

And often, these issues only come to light when someone else reviews the numbers—by which point they’re harder to fix.

You Lose Visibility Without Realising It

When bookkeeping is inconsistent or rushed, your numbers become harder to trust.

That means:

You’re not fully confident in your profit

You can’t clearly see where money is going

You hesitate when making decisions

And that has a knock-on effect.

You might delay:

Hiring

Investing

Expanding

Not because the business isn’t ready—but because you don’t have clear enough information to act confidently.

The “Clean-Up Cost” Later On

This is where many businesses feel the impact most.

If your bookkeeping isn’t kept up to date or accurate:

Your accountant may need extra time correcting it

You may be charged more at year-end

You may face delays in submitting accounts or returns

In some cases, businesses end up paying significantly more to fix issues than they would have paid to keep things running smoothly in the first place.

It’s Not About Doing Nothing—It’s About Doing the Right Things

This isn’t about stepping away from your finances.

In fact, understanding your numbers is one of the most valuable things you can do as a business owner.

But there’s a difference between:

Being informed, and

Doing everything yourself

The goal is to have:

Clear, up-to-date information

Confidence in your numbers

Time to focus on running your business

When It Makes Sense to Get Support

There’s no single “right moment”—but there are clear signs it might be time:

You’re regularly behind on your bookkeeping

It’s taking up more time than you expected

You’re unsure if everything is correct

You’re making decisions without clear financial data

Getting support doesn’t just solve a problem—it creates space.

Space to focus, to grow, and to run your business more effectively.

Key Takeaways

Doing your own bookkeeping might feel cost-effective at first—but the hidden costs can build over time.

In time, stress, and missed opportunities—not just money.

The real question isn’t:

👉 “Can I do this myself?”

It’s:

👉 “Is this the best use of my time and energy?”

CTA

If your bookkeeping is taking up more time than it should—or starting to feel like a source of stress—it may be time to rethink how it’s handled.

Disclaimer

The information in this article is for general guidance only and does not constitute financial, tax, or legal advice. While we aim to keep content accurate and up to date, rules and regulations can change and individual circumstances vary.

You should always seek advice from a qualified accountant or professional adviser regarding your specific situation before making any decisions.